Headlines Vs. Trendlines | Seattle’s Housing Market May Be Leading The Next Recovery

Are you planning your next real estate move but wondering where the market stands? Let’s explore the data.

At first glance, the latest S&P Cotality Case-Shiller Home Price Index might appear discouraging. Seattle recorded the largest year-over-year home price correction (-2.3%) among the nation’s twenty largest metropolitan markets through April 2026, prompting headlines that suggest the region is falling behind.

However, the opposite may be true. Seattle has often been an early-cycle market—one of the first to accelerate during periods of expansion and one of the first to recalibrate when conditions change. Today’s moderation reflects a healthy return to price discovery following years of exceptional appreciation, rather than a deterioration in the region’s long-term fundamentals.

In fact, when viewed alongside several other economic indicators, a far more compelling story emerges.

The U.S. Bureau of Economic Analysis recently reported that Washington posted the fastest economic growth in America during the first quarter of 2026, with gross domestic product expanding at an annualized 4.5%, more than twice the national average of 2.1%. That performance was driven largely by Washington’s outsized technology sector, reinforcing the state’s position as one of the world’s leading innovation economies.

At the same time, the Puget Sound region is experiencing a resurgence in commercial real estate activity as artificial intelligence companies expand aggressively throughout Seattle and Bellevue. Microsoft, Amazon, OpenAI, Google, Meta, NVIDIA, AI2, and a growing ecosystem of AI startups continue investing billions of dollars in cloud infrastructure, engineering talent, and office space. Industry analysts project 2026 could become a record year for AI-related office absorption in the region as companies secure space ahead of future hiring.

This broader context aligns closely with the findings of the 2026 RSIR Mid-Year Market Barometer®, where fourteen experienced market leaders reported a Composite Market Sentiment Index of 3.12, reflecting cautious optimism and growing confidence that buyers and sellers are adapting to a more balanced marketplace. Rather than describing a market in decline, brokers consistently identified expanding inventory, AI-driven wealth creation, equity market strength, and the Great Wealth Transfer as long-term catalysts supporting future demand, even as affordability challenges and evolving tax policies encourage greater pricing discipline. These seemingly contradictory trends form what RSIR describes as the Barbell Market.

On one end are headwinds including mortgage affordability, public policy uncertainty, and increasingly analytical buyers. On the other are powerful structural tailwinds including record economic growth, AI investment, expanding office leasing, unprecedented wealth creation, and one of the largest intergenerational wealth transfers in history.

Rather than canceling each other out, these opposing forces are producing something even more valuable than rising home prices: Liquidity.

Inventory is improving. Buyers are returning. Negotiations are increasing. Transactions are accelerating. This is precisely what healthy markets are supposed to do.

If the first half of 2026 was defined by kicking the beehive, the second half is expected to reveal where the bees choose to land. As consumers adapt to changing market conditions, more buyers and sellers are finding common ground, creating a marketplace that is increasingly transparent, efficient, and active.

The silver lining behind Seattle’s recent price correction is that it may ultimately prove to be the foundation for the region’s next chapter of sustainable growth. Strong economic fundamentals, expanding AI investment, record GDP growth, and improving market liquidity suggest that the Puget Sound housing market is not losing momentum—it is recalibrating and pricing in recent turbulence from prior reporting in March and April (the depths of political and inflationary dynamics).

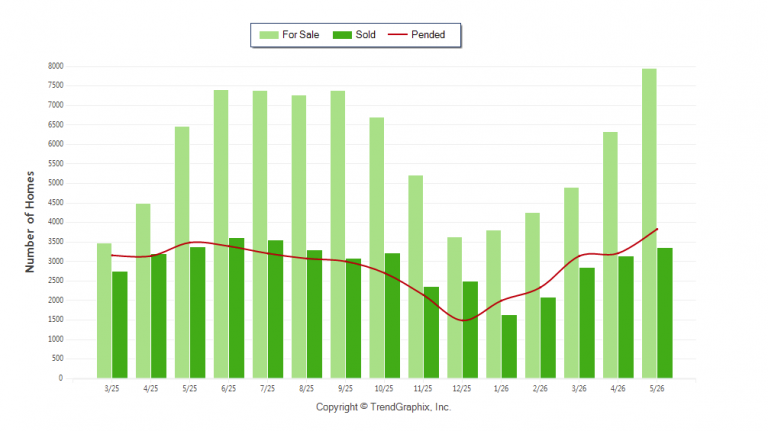

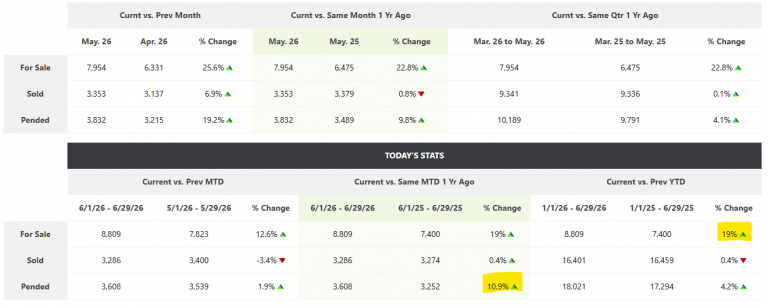

A quick look at how the markets shaped up since the S&P reporting period of April illustrates improvement (data is resale of single-family homes for the four-county region similar to how S&P calculates it’s index):

We can see a sizable spike of inventory rising 19% year-over-year, but a significant rebound of sales so far in the month of June, increasing 10.9% year-over-year, and gaining more in the past month than in the trending so far in 2026. That’s improving buyer demand responding to more inventory, sharper pricing, better negotiation leverage, and rising consumer confidence overall.